Conversation Interest rates

Comment: How rising interest rates are affecting UK businesses

Published on: 22 August 2023

Writing for The Conversation, Dr Erwei Xiang looks at how UK businesses are being affected by rising interest rates.

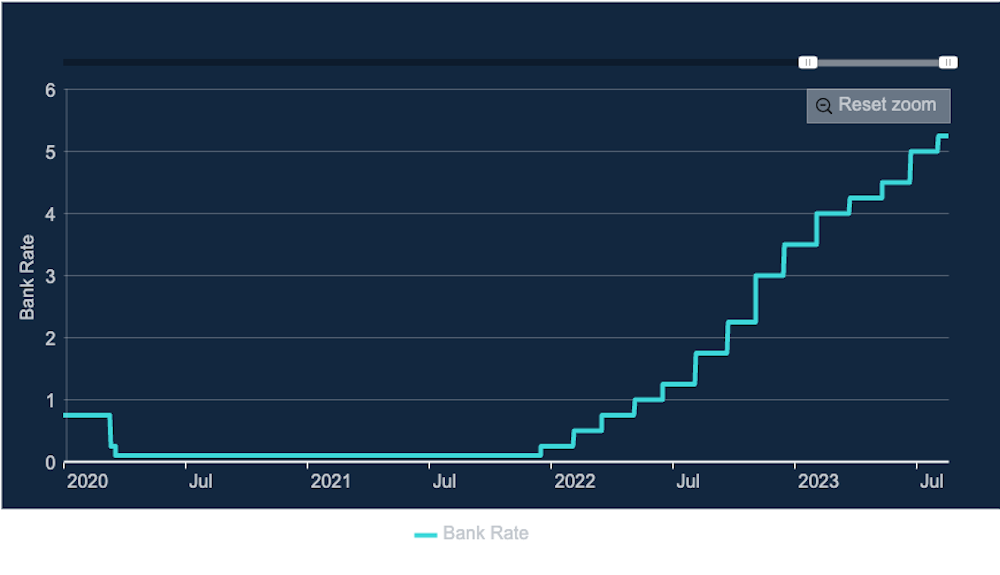

From chip shops to tech start-ups, and even large, well-established companies, rising interest rates have had an impact right across the business world. After 14 consecutive base rate hikes by the Bank of England since 2021, this is causing particular problems for companies with a lot of debt.

We recently saw the chaos this can cause when English utility Thames Water nearly collapsed under the weight of its debt and had to seek emergency funding from its shareholders earlier this year.

More recently, budget retailer Wilko’s borrowing not only affected the business and its shareholders, but also its employees when its recent collapse put 12,500 jobs at risk.

Similar problems could arise among many other companies and industries. Financial markets expect the bank base rate – which dictates the rates on many types of loans – will keep climbing: it’s currently forecast to peak between 5.75% and 6% by the start of 2024. And the total value of UK business loans is also expected to rise to an estimated £513 billion as of 2023. This is £78 billion higher than in 2018, an increase of 18%.

Company insolvencies have already jumped by 40% over the year to May 2023 in England and Wales – the highest level since monthly records began in January 2019. And significant debt problems within an industry or even one firm can cause a domino effect across the UK economy.

Research shows the effects of an insolvency or bankruptcy can spread to a firm’s trading partners. Wilko started to defer supplier payments and extend the timeframe in which it settles invoices last year to try to ease pressure on its cash flow as it struggled to manage its debts.

So, with interest rates likely to continue to rise, being able to tell if another company or industry is at risk is important for customers, employees, investors and other connected businesses such as suppliers.

The rising cost of business borrowing

The average cost of new borrowing from banks by private non-financial companies was 6.36% in June 2023, more than 4 percentage points above the December 2021 rate of 2.03% (when the Bank of England base rate increases began). For small and medium-sized enterprise (SMEs), new loan rates increased from 6.86% in May to a record high of 7.13% in June (compared with 2.51% in December 2021).

Companies already holding debt that’s not on a fixed rate of interest could also see an increase in the interest owed to their lender. This could come as a shock since UK interest rates were 1% or less for more than 13 years from February 2009 to June 2022. During this time, the pressure of debt on borrowers was light or negligible.

The base rate has recently climbed from low levels

Companies that got used to being able to borrow at a low cost are now starting to feel the pinch, or even come under extreme pressure if they are heavily indebted. This is what worsened the financial position of UK utility Thames Water. When the company was privatised in 1989, it had no debt. But over the years it borrowed heavily to fund new investments.

Generally speaking, debt is a prudent low-cost source of finance with low interest rates fixed for the long term. But Thames Water borrowed too much. It had £14 billion in debt by the end of June 2023, which amounted to 80% of the value of the business and made it the most heavily indebted of England and Wales’ water companies, according to analysts. Its loan repayments were not only linked to the bank base rate, but also inflation, which has also spiked over the past year. This triggered fears about the company’s ability to continue to service its debts.

Thames Water was lucky, in a sense – it avoided being nationalised because it was able to secure timely funding from its shareholders. But the situation revealed the extent of the iceberg under the water in this industry. Shortly afterwards, another English utility, Southern Water, announced it would not pay dividends until at least 2025 after its credit rating was downgraded. This shows investors, lenders and credit ratings agencies are getting more nervous about debt-related trends within industries.

Businesses can help to ease such concerns by being transparent. Research shows that the more firms disclose financial and non-financial information, the more likely they are to be able to secure loans and access lower rates. This also applies to companies that are more open with external partners by sharing resources and knowledge to enhance innovation. The more information a bank has, the more comfortable it will be about lending to a company. It also reduces the bank’s own risk rating, allowing it to lend more and offer lower rates.

What to look out for in the current environment

Business leaders that are addressing rising interest rates head-on may announce adjustments to their growth or expansion plans, especially if a plan previously relied heavily on debt. They may also consider different sources of finance. The UK water regulator, for example, has called on utilities to consider the role of equity funding (for example, selling shares) and not just debt in financing new investment.

A company’s ratio of debt versus assets will also tell you how much it holds in debt. A “good” debt ratio is around 1 to 1.5, but the ideal can vary by industry. Manufacturers, for example, tend to need a lot of equipment and so may have ratios greater than 2.

More interest rate rises will pile pressure on companies, employees and the economy. But by anticipating the impact on their debt and being more open about their current state and future plans, businesses can help to minimise the pain.

Erwei (David) Xiang, Senior Lecturer (Associate Professor) in Accounting, Newcastle University

This article is republished from The Conversation under a Creative Commons license. Read the original article.